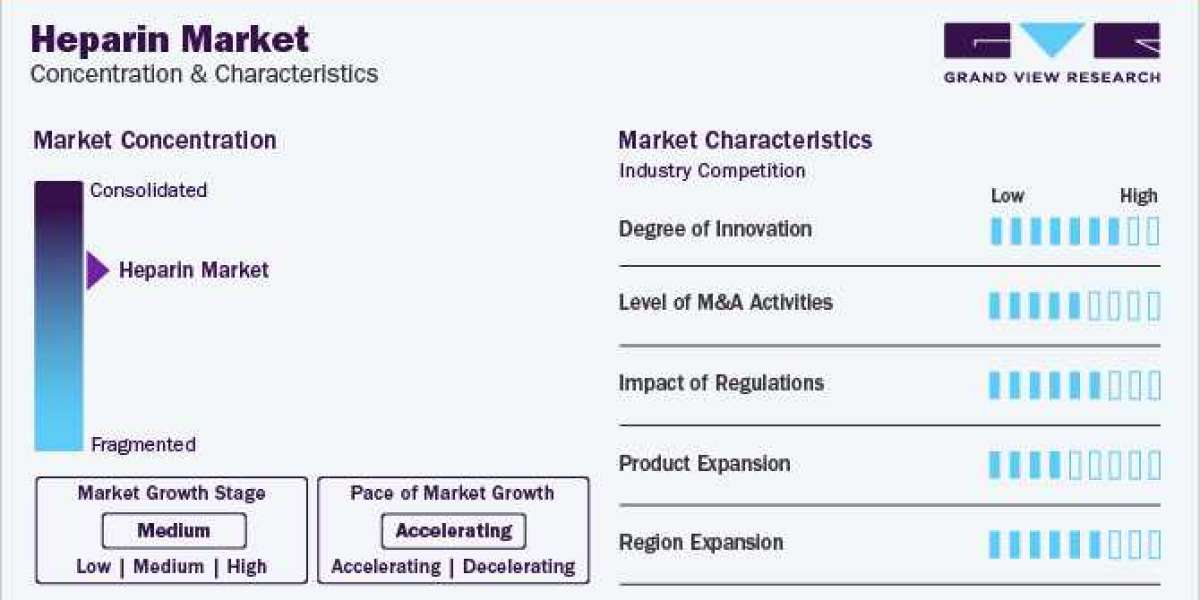

Heparin Industry Overview

The global heparin market size was estimated at USD 7.56 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 2.7% from 2024 to 2030. The increasing prevalence of chronic diseases is a major factor in market growth. According to a WHO article published in September 2023, Noncommunicable diseases (NCDs), also known as chronic diseases, cause about 41 million deaths annually, of which 17.9 million deaths are attributed to cardiovascular diseases (CVD). Cancer causes 9.3 million deaths, chronic respiratory diseases lead to 4.1 million deaths, and diabetes contributes to 2 million deaths, including those from diabetes-related kidney diseases. Growing demand for whole blood and blood components transfusion, increasing geriatric population and high usage of plasma in the pharmaceutical industry are factors expected to drive this market’s growth.

Growing demand for whole blood and blood components transfusion is boosting the demand for the heparin market. Many places worldwide are unable to meet their demand of blood. People are working hard to make more individuals aware of the importance of donating blood. According to an NCBI article published in October 2023, in the U.S. alone, someone needs blood every two seconds, and these transfusions save many lives. As 62 out of 171 countries have a 100% voluntary unpaid blood donation system, it is evident that maintaining an adequate and safe blood supply is challenging. The demand for heparin is set to rise alongside these initiatives, ensuring the success of transfusions and ultimately saving more lives.

Gather more insights about the market drivers, restrains and growth of the Heparin Market

Detailed Segmentation:

Application Insights

The Coronary Artery Disease (CAD) segment held the largest revenue share of 23.4% in 2023. CAD involves the narrowing of coronary arteries, leading to reduced blood flow to the heart. According to an NCBI article published in August 2023, CAD, considered the most common heart disease, involves atheromatous changes in heart-supplying vessels, leading to various clinical disorders. As a leading cause of mortality in the U.S., CAD necessitates interventions like heparin, which plays a crucial role in preventing blood clot formation and managing acute coronary events. The focus on initial risk factor evaluation aligns with the comprehensive approach to CAD management, where heparin serves as a key component.

Atrial fibrillation segment is estimated to register a significant CAGR from 2024 to 2030. Atrial fibrillation, a common heart rhythm disorder, necessitates anticoagulant therapy to prevent blood clot formation. According to the CDC, atrial fibrillation is estimated to be reported in 12.1 million people in the U.S. by 2030, and is an underlying cause of death in 26,535 people. Additionally, it was revealed that 15% - 20% of stroke patients also suffer from arrhythmia, which calls for the use of blood thinners as a form of treatment. The main signs and symptoms of this illness are fatigue, weakness, dizziness, shortness of breath, chest discomfort, palpitations, and lightheadedness. These aspects are expected to boost the demand for heparin.

Regional Insights

North America dominated the market and accounted for 38.6% share in 2023, driven by a rising patient awareness, high disease burden, proactive government measures, technological advancements, and improvements in healthcare infrastructure. The presence of key players in this region is a significant propeller of market growth. According to the CDC article published in May 2023, the prevalence of a heart disease is the leading cause of death in the U.S., resulting in one death every 33 seconds and serving as a significant growth driver for the market. The high incidence of CVD underscores the crucial role of heparin, a key anticoagulant, in managing and treating cardiovascular conditions, contributing to the market's sustained demand.

Type Insights

Low Molecular Weight Heparin (LMWH) segment accounted for the largest revenue share of 63.7% in 2023. LMWH is an anticoagulant that is administered intravenously or subcutaneously and is majorly used in the treatment of prophylaxis of venous thromboembolic disease, deep vein thrombosis, and pulmonary embolism. Some examples of LMWH are enoxaparin and dalteparin. According to the NCBI article published in October 2023, a substantial proportion of patients (77%) received prophylaxis with LMWH, and the findings of the study indicate that LMWH was associated with a significantly lower rate of venous thromboembolism compared to unfractionated heparin. This highlights the distinctive role of LMWH in reducing the risk of venous thromboembolism in individuals undergoing such medical procedures.

Route of Administration Insights

Subcutaneous administration of heparin accounted for the largest revenue share of 65.4% in 2023. The major advantage of subcutaneous injections is that they can be easily administered at home with little knowledge and expertise, making it a cost-effective alternative. According to NCBI article published in August 2023, the elevated bioavailability of Enoxaparin, with 90% of the drug being accessible through subcutaneous administration, stands as a significant growth driver for the subcutaneous segment. This advantage positions Enoxaparin as a favorable choice over traditional heparin, emphasizing the efficient and potent delivery achieved through the subcutaneous route.

End-use Insights

The outpatient segment accounted for the largest revenue share of 61.1% in 2023. Outpatients hold a distinct advantage over other healthcare options, primarily driven by the significant reduction in hospital-related expenses, including admission costs and other hospitality-related charges. The prominent share of this segment is attributed to cost-effectiveness, enhanced service availability, and the convenience heparin offers to patients. The emphasis on low costs and increased accessibility contributes to the dominance of this segment, reflecting a healthcare trend prioritizing economic efficiency and patient convenience.

Source Insights

The porcine segment accounted for the largest revenue share of 90.0% in 2023. This can be attributed to porcine’s wide usage in heparin production, especially LMWH, such as enoxaparin. Porcine heparin (180-220 units/mg) also has a higher anticoagulant activity when compared to bovine (130-150 units/mg), owing to its strong pharmacological and biochemical effects. Porcine heparins are 30%-50% more potent than bovine heparins. Furthermore, porcine heparin is easier to neutralize in adverse situations.

Browse through Grand View Research's Category Pharmaceuticals Industry Research Reports.

- The global kidney cancer drugs market size was valued at USD 6.25 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 6.9% from 2024 to 2030.

- The global hyperlipidemia drugs market size was valued at USD 23.1 billion in 2023 and is projected to grow at a compound annual growth rate (CAGR) of 2.8% from 2024 to 2030.

Key Companies Market Share Insights

- Pfizer Inc.; LEO Pharma A/S; and Sanofi are some of the dominant market players.

- Pfizer, Inc. is a pharmaceutical company based in the U.S. and founded in 1849. It manufactures products for curing a wide range of medical disciplines, including diabetes, immunology, cardiology, oncology, dermatological diseases, rare diseases, inflammatory diseases, oncology, and vaccines.

- Sanofi was incorporated in 1994 and is headquartered in France. It engages in RD, manufacturing g, and marketing of therapeutic solutions, comprising diabetes, human vaccines, innovative drugs, consumer healthcare, CVD, internal medicine, immunology, neurology, thrombosis, oncology, arthritis, central nervous system, osteoporosis, primary healthcare, vaccines, animal health, and Genzyme.

- Braun Medical, Inc.; Sandoz (Novartis AG); and Aspen Holdings are some of the emerging market players

- Novartis AG is a Swiss-based multinational company involved in RD, manufacturing, and marketing of healthcare products. The company was formed following the merger of Sandoz Laboratories, Inc. and Ciba-Geigy AG. It is a publicly held organization and operates through two segments: Innovative Medicines and Sandoz.

- Braun Medical, Inc. is involved in developing, manufacturing, and marketing innovative medical products services. The company was established in 1839 and is headquartered in Germany.

Key Heparin Companies:

- Pfizer Inc.

- LEO Pharma A/S

- Dr. Reddy’s Laboratories, Ltd.

- GlaxoSmithKline plc

- Sanofi

- Aspen Holdings

- Fresenius SE Co., KGaA

- B. Braun Medical, Inc.

- Sandoz (Novartis AG)

Heparin Market Segmentation

Grand View Research has segmented the global heparin market based on type, route of administration, application, end-use, source, and region:

Heparin Type Outlook (Revenue, USD Million, 2018 - 2030)

- Low Molecular Weight Heparin

- Ultra-low Molecular Weight Heparin

- Unfractionated Heparin

Heparin Route of Administration Outlook (Revenue, USD Million, 2018 - 2030)

- Intravenous

- Subcutaneous

Heparin Application Outlook (Revenue, USD Million, 2018 - 2030)

- Venous Thromboembolism

- Atrial Fibrillation

- Renal Impairment

- Coronary Artery Disease

- Others

Heparin End-use Outlook (Revenue, USD Million, 2018 - 2030)

- Outpatient

- Inpatient

Heparin Source Outlook (Revenue, USD Million, 2018 - 2030)

- Porcine

- Bovine

- Others

Heparin Regional Outlook (Revenue, USD Million, 2018 - 2030)

- North America

- U.S.

- Canada

- Europe

- UK

- Germany

- France

- Italy

- Spain

- Denmark

- Sweden

- Norway

- Asia Pacific

- China

- Japan

- India

- Australia

- Thailand

- South Korea

- Latin America

- Brazil

- Mexico

- Argentina

- Middle East Africa

- South Africa

- Saudi Arabia

- UAE

- Kuwait

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.

Recent Developments

- In June 2023, Techdow USA Inc., part of the Hepalink Group, launched Enoxaparin Sodium (Enoxaparin). This crucial product, available in seven popular pre-filled syringe formats, addresses the critical need for outpatient treatment and prevention of harmful blood clots.

- In July 2023, Endo International's Par Sterile Products business commenced the shipment of bivalirudin injection in a convenient ready-to-use 250 mg/50 mL single-use vial. This product stands out as the sole liquid format of bivalirudin available in the U.S.

- In August 2023, The FDA has approved Delcath Systems, Inc.'s HEPZATO KIT for treating adult patients with metastatic uveal melanoma and unresectable hepatic metastases.

- In November 2023, the FDA has approved CorMedix's antimicrobial drug to reduce catheter-related bloodstream infections in kidney disease patients, marking the company's first commercial product launch.