Mobility - Voice and Data Procurement Intelligence

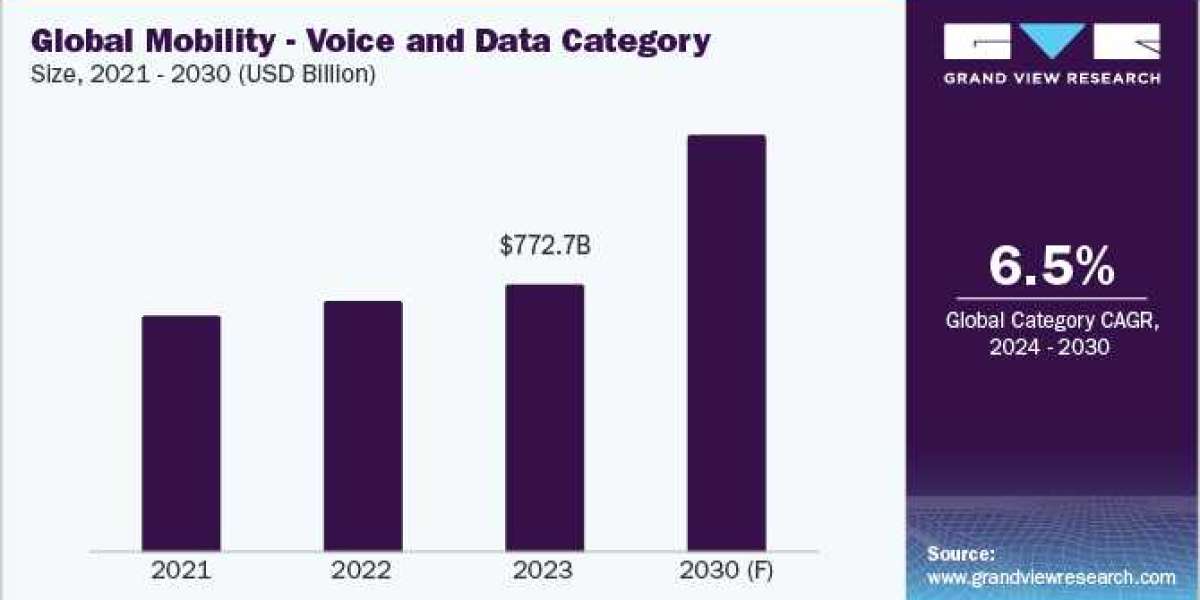

The mobility - voice and data category is projected to witness growth at a CAGR of 6.5% from 2024 to 2030. In 2023, Asia Pacific accounted for the largest share (32%) of the global category. Key drivers of this region include a consistent increase in the business/enterprise subscriber base for voice and data, deployment of VoNR (5G) network by key players, and a shift towards virtualization and software-defined networking (SDN). Asia Pacific is also anticipated to witness the fastest growth rate during the forecast period, due to the increasing need for business agility, focus on cost efficiency by businesses, and adoption of digital technologies such as Internet of Things (IoT), cloud computing, and Artificial Intelligence (AI).

In 2023, North America held the second-largest share of the global market. The key growth drivers include large coverage of 5G networks by key service providers, increasing adoption of edge computing infrastructure, and focus on sustainability initiatives. Key driving factors for Europe include extensive voice and data coverage in remote areas owing to government initiatives, increasing deployment of high-speed fiber optic networks, and focus on cyber security.

Key technologies driving the growth of this category include AI and Machine Learning (ML), quantum computing, edge computing, cloud computing and virtualization, and IoT integration. Edge computing is used to enhance the processing and storage of data, reduce latency, improve bandwidth, and enhance customer experience. By using a distributed network architecture, this technology processes real-time data at quicker speeds. Similarly, the use of virtualization enhances network infrastructure utilization, reduces hardware costs, and improves agility, by using virtual machines in place of hardware resources.

Key service providers of mobility - voice and data services compete based on various factors such as subscription rates, innovations in technologies and services, user experience, scalability of services, and data privacy and security. Clients (specifically business customers) consider factors such as service type (4G/5G), service deployment (cloud/on-premise), service transmission (wireline/wireless), service reliability (uptime/downtime), service speeds (download speeds typically range from 100 Mbps to 1 Gbps), and extent of network coverage (based on area covered). Specifically, business customers may also look for add-on features such as call routing, data integration linking, caller identification, and call monitoring.

Order your copy of the Mobility - Voice and Data category procurement intelligence report 2023-2030, published by Grand View Research, to get more details regarding day one, quick wins, portfolio analysis, key negotiation strategies of key suppliers, and low-cost/best-cost sourcing analysis

Mobility - Voice and Data Sourcing Intelligence Highlights

- The mobility - voice and data category comprises a moderately consolidated landscape, with a few top competitors accounting for a significant portion of the market share.

- Countries such as Israel and Italy are the countries that offer mobility - voice and data services at low cost owing to cheap labor costs, low technology costs, high smartphone adoption, intense market competition, deployment of penetration pricing, and robust government initiatives.

- Buyers in the category possess medium-to-low negotiating capability due to the moderately consolidated market landscape. Moreover, buyers have specific limitations when switching to an alternative service provider.

- Network infrastructure, labor, hardware and software, spectrum acquisition, licensing and compliance, and other costs are the key cost components of this category. Other costs include sales and marketing, general and administrative, rent and utilities, insurance, logistics, and taxes.

List of Key Suppliers

- ATT Inc.

- Broadcom Inc.

- Charter Communications, Inc.

- Cisco Systems, Inc.

- Comcast Corporation

- Deutsche Telekom AG

- Huawei Technologies Co., Ltd.

- Lumen Technologies, Inc.

- Orange S.A.

- Telefónica S.A.

- Verizon Communications Inc.

- Vodafone Group Plc.

Browse through Grand View Research’s collection of procurement intelligence studies:

- Disposable Medical Gloves Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement Operating Model, Competitive Landscape)

- Loyalty Programs Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement Operating Model, Competitive Landscape)

- Helium Procurement Intelligence Report, 2023 - 2030 (Revenue Forecast, Supplier Ranking Matrix, Emerging Technologies, Pricing Models, Cost Structure, Engagement Operating Model, Competitive Landscape)

Mobility - Voice and Data Procurement Intelligence Report Scope

- Mobility - Voice and Data Category Growth Rate : CAGR of 6.5% from 2024 to 2030

- Pricing Growth Outlook : 5% - 10% increase (Annually)

- Pricing Models : Penetration pricing, subscription-based pricing, usage-based pricing, tiered pricing, cost-plus pricing, and competition-based pricing

- Supplier Selection Scope : Cost and pricing, past engagements, productivity, geographical presence

- Supplier Selection Criteria : Geographical service provision, industries served, years in service, employee strength, revenue generated, key clientele, regulatory certifications, voice services, data services, cloud and hosting services, managed network services, unified communication services, and others

- Report Coverage : Revenue forecast, supplier ranking, supplier positioning matrix, emerging technology, pricing models, cost structure, competitive landscape, growth factors, trends, engagement, and operating model

Brief about Pipeline by Grand View Research:

A smart and effective supply chain is essential for growth in any organization. Pipeline division at Grand View Research provides detailed insights on every aspect of supply chain, which helps in efficient procurement decisions.

Our services include (not limited to):

- Market Intelligence involving – market size and forecast, growth factors, and driving trends

- Price and Cost Intelligence – pricing models adopted for the category, total cost of ownerships

- Supplier Intelligence – rich insight on supplier landscape, and identifies suppliers who are dominating, emerging, lounging, and specializing

- Sourcing / Procurement Intelligence – best practices followed in the industry, identifying standard KPIs and SLAs, peer analysis, negotiation strategies to be utilized with the suppliers, and best suited countries for sourcing to minimize supply chain disruptions